A negociação de opções binárias permite que traders de todos os níveis de habilidade especulem facilmente nos mercados. No entanto, a facilidade de negociação que estes instrumentos financeiros proporcionam é apenas uma das muitas vantagens que oferecem.

Talvez a vantagem mais significativa dos binários de negociação seja o risco limitado de desvantagem que eles oferecem, independentemente de você estar comprando ou vendendo. Assim, você sempre sabe o quanto pode ganhar (ou perder).

No entanto, para negociar binários, primeiro você deve abrir uma conta de Opções Binárias com um corretor. Não há escassez de corretores de opções binárias, mas há apenas um punhado de corretores reconhecidos com os quais os negociadores preferem se inscrever.

O processo de criação de conta pode diferir ligeiramente de corretor binário para corretor, mas as etapas que você precisa seguir são essencialmente as mesmas. Aqui está um guia sobre como finalizar o registro de opções binárias e começar a negociar binárias.

Como abrir uma conta de opções binárias:

Você pode começar a negociar com um corretor de Opções Binárias confiável completando o registro de Opções Binárias em quatro etapas fáceis.

Etapa #1: conecte um dispositivo à Internet

As opções binárias são instrumentos mais comumente negociados em plataformas binárias negociadas online. Para criar uma conta e posteriormente especular, você precisará de acesso a um computador ou telefone conectado à internet.

Além de ter um telefone ou computador que pode se conectar à internet, você deve ter uma conexão de internet estável. Considere obter uma conexão de um provedor de serviços de Internet confiável, já que velocidades lentas de Internet e desconexões podem custar caro, por exemplo, se você não encerrar um período de troca.

Etapa #2: Escolha um corretor de opções binárias confiável

Mais de 100 mercados

- Aceita clientes internacionais

- Pagamentos elevados 95%+

- Plataforma profissional

- Depósitos rápidos

- Negociação Social

- Bônus grátis

Mais de 100 mercados

- Min. depósito $10

- $10,000 demo

- Plataforma profissional

- Lucro alto até 95%

- Retiradas rápidas

- Sinais

Mais de 300 mercados

- Depósito mínimo $10

- Conta de demonstração gratuita

- Alto retorno até 100% (no caso de uma previsão correta)

- A plataforma é fácil de usar

- Suporte 24/7

Mais de 100 mercados

- Aceita clientes internacionais

- Pagamentos elevados 95%+

- Plataforma profissional

- Depósitos rápidos

- Negociação Social

- Bônus grátis

a partir de $50

(Aviso de risco: negociar é arriscado)

Mais de 100 mercados

- Min. depósito $10

- $10,000 demo

- Plataforma profissional

- Lucro alto até 95%

- Retiradas rápidas

- Sinais

a partir de $10

(Aviso de risco: negociar é arriscado)

Mais de 300 mercados

- Depósito mínimo $10

- Conta de demonstração gratuita

- Alto retorno até 100% (no caso de uma previsão correta)

- A plataforma é fácil de usar

- Suporte 24/7

a partir de $10

(Aviso de risco: seu capital pode estar em risco)

Nem todo corretor permite negociação binária. Portanto, mesmo que você tenha uma conta de negociação em uma corretora, talvez não consiga usar a mesma corretor para negociar opções binárias.

Você precisará selecionar um corretor de opções binárias especializado para especular usando binários. Embora a maioria desses corretores permita que clientes da maioria dos países usem sua plataforma, há uma chance de que o corretor que você escolheu não permita que os negociadores de seu país negociem em sua plataforma.

Você deve ter isso em mente e garantir que a corretora permitirá que você use sua plataforma antes de abrir uma conta. Isso vai economizar muito tempo e esforço.

Além disso, é essencial que você escolha um corretor bem regulamentado que permita negociar binários em ativos e mercados com os quais você está familiarizado. Mudar para ativos de negociação em mercados com os quais você não está familiarizado aumenta as chances de perder dinheiro ao negociar. Por fim, você deve certificar-se de que a corretora escolhida oferece seus serviços a preços competitivos. Pagar taxas um pouco mais altas pode não parecer um problema; no entanto, os custos somam uma grande quantidade à medida que você faz mais e mais negociações.

Com esses fatores em mente, listamos três dos melhores corretores de opções binárias do mercado com os quais você pode se inscrever.

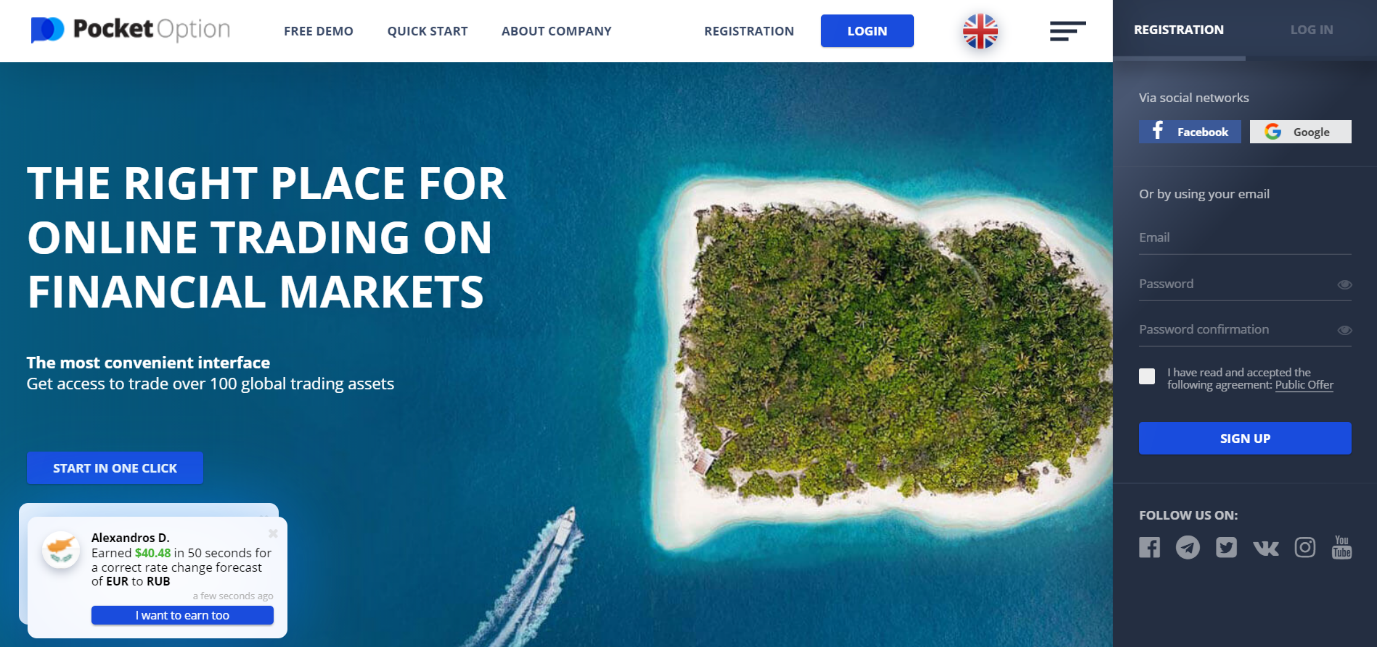

Opção de bolso #1

Fundada em 2017, Pocket Option é outra corretora reconhecida que permite a negociação de binários. Com um processo de registro de opções binárias simples, mais de 130 ativos para negociar e disponibilidade de serviço na maioria dos países, é difícil escolher outros corretores em vez de Opção de bolso.

Embora o depósito mínimo seja $50, o valor mínimo de negociação é $1. Mas talvez a melhor coisa sobre a plataforma é que você pode se inscrever e usar a conta demo gratuitamente, sem qualquer compromisso. Isso o torna a plataforma perfeita para traders novatos.

A plataforma também oferece recursos como negociação social e hospeda torneios com prêmios variados. A interface da web fácil de usar e o aplicativo móvel tornam a negociação conveniente.

(Aviso de risco: seu capital pode estar em risco)

#2 Quotex.io

Quotex.io é um corretor de opções binárias relativamente novo - foi fundada em 2020. Mas rapidamente se estabeleceu como uma corretora líder. Além disso, é membro de o IFMRRC, tornando-se uma plataforma regulamentada e confiável para os comerciantes.

A plataforma impõe restrições de pagamento aos comerciantes dos EUA, Canadá, Hong Kong e Alemanha. No entanto, contanto que você tenha mais de 18 anos de idade, pode depositar em sua conta usando criptomoeda e comércio.

O valor mínimo de depósito é $10, e a plataforma também oferece uma conta de demonstração, permitindo que os traders pratiquem a negociação em tempo real sem ter que arriscar nenhum capital. O rendimento pode ser muito alto até 90% +. Pessoalmente, gosto dessa plataforma de negociação, ela funciona bem e rapidamente.

(Aviso de risco: seu capital pode estar em risco)

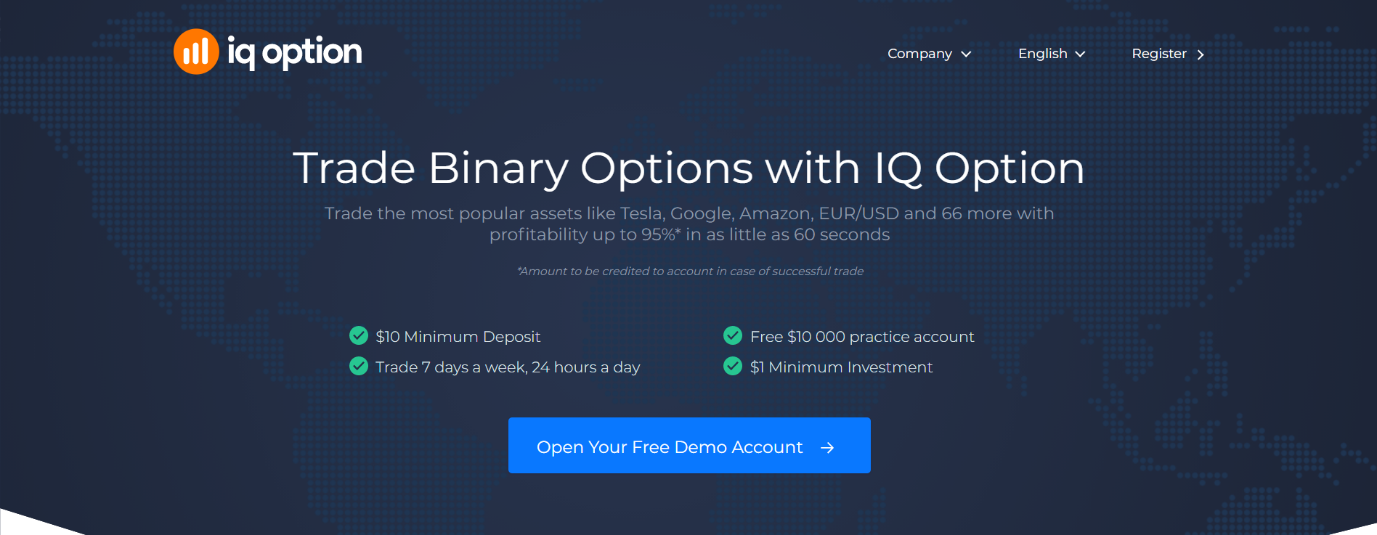

Opção IQ #2

IQ Option é uma das corretoras de opções binárias mais populares, com mais de 40 milhões de usuários registrados. A corretora é regulamentada pelo Comissão de Valores Mobiliários do Chipre e também a Autoridade de Serviços Financeiros das Seychelles.

É considerado o corretor preferido por traders novatos em todo o mundo. O depósito mínimo é $10 para uma conta padrão. Você instantaneamente obtém acesso a mais de 350 ativos para negociar. A corretora também oferece contas VIP com benefícios adicionais para negociadores que depositem mais de $1900 em dois dias.

Não há bônus de depósito, mas a corretora realiza vários torneios de negociação. Os vencedores recebem prêmios que variam de $100 a $100.000.

A opção IQ está disponível em mais de 213 países. No entanto, a plataforma não está disponível para comerciantes em países como Estados Unidos, Rússia, Canadá, Austrália, França, Japão, Bélgica e alguns países do Oriente Médio, devido a regulamentações mais rígidas.

Como Quotex.io, IQ Options também oferece uma conta demo que você pode usar para praticar estratégias de negociação sem qualquer risco.

(Aviso de risco: seu capital pode estar em risco)

Etapa #3: Abra uma conta e financie-a

Depois de escolher um dos muitos corretores de opções binárias, você deve fazer uma conta com eles. Para abrir uma conta em qualquer corretora, você precisará atender aos requisitos de conta da corretora. Você precisará fornecer o seu:

- Primeiro e último nome

- País de Residência

- Moeda de negociação preferida

- método de pagamento preferido

- Endereço de e-mail e

- Senha

Algumas corretoras também pedem seu número de telefone. Ele pode ser usado para confirmar sua identidade, para autenticação de dois fatores ou para fornecer suporte por telefone, se necessário.

Embora a maioria dos corretores não peça suas informações de pagamento durante o processo de registro de opções binárias, pode ser necessário inseri-las.

Verificando sua identidade:

Depois de fornecer suas informações básicas, o corretor solicitará que você verifique sua identidade. Isso requer que você carregue uma cópia de sua identificação de estado para o portal seguro do corretor. Algumas corretoras também precisam que os clientes participem de uma chamada de vídeo para verificação de identidade.

As corretoras verificam a identidade de cada comerciante para evitar várias coisas:

- Fraude: Indivíduos com menos de 18 anos, comerciantes que moram em determinados países não têm permissão para acessar a plataforma para evitar possíveis fraudes.

- Roubo de identidade: Verificar todos os usuários da plataforma reduz as chances de hackers roubarem e se passarem por um usuário com sucesso.

Os processos de verificação geralmente levam menos de três dias. O inconveniente de esperar para ser verificado pela corretora ajuda muito a manter a plataforma e os negociadores seguros.

Dito isso, algumas corretoras não exigem verificação e permitem que você comece a negociar assim que inserir suas informações básicas e definir uma senha.

(Aviso de risco: seu capital pode estar em risco)

Etapa #4: Use sua conta demo de negociação de opções binárias ou conta real

A maioria dos corretores de opções binárias dá a você acesso a duas contas: uma conta ao vivo e uma conta demo. A conta de demonstração permite que você faça negociações com “demo” dinheiro em tempo real.

Não há necessidade de baixar e instalar o software para usar esta conta. Ao acessá-lo, você será redirecionado para uma página que dá acesso à plataforma com o dinheiro de demonstração.

As contas de demonstração são usadas para praticar estratégias de negociação sem a necessidade de gastar capital real. Usar uma conta demo é a maneira mais conveniente de testar estratégias e aprender a negociar se você for um iniciante.

Para usar a conta ativa, você deve financiá-la usando métodos como transferência eletrônica. Em seguida, você pode usar os fundos da conta de negociação para fazer negócios no mercado ao vivo.

Conta normal vs conta de negociação gerenciada

A conta de opções binárias permite negociar derivativos financeiros na plataforma da corretora, mas também há a chance de obter um conta de opções binárias gerenciadas. Este tipo de conta é administrada por um profissional que cuida dos seus investimentos ou dá consultoria sobre investimentos. Pela nossa pesquisa, pode ser muito arriscado assumir uma conta gerenciada porque geralmente não há profissionais na empresa da corretora que possam fazer negociações lucrativas.

Diferentes tipos de contas de opções binárias explicados:

Escolher um tipo de conta é um desafio, especialmente quando você não sabe que tipo de negociação deve fazer. Depois de verificar isso, será mais fácil escolher o tipo de conta. Aqui estão os tipos de contas mais comuns para negociação de opções binárias.

A conta virtual (demonstração)

Você acabou de iniciar sua jornada de investimento, mas tem medo de investir dinheiro real? Não se preocupe, pois as contas virtuais podem ajudá-lo a acabar com esse medo. Antes de investir em opções binárias com dinheiro real, você pode testar suas estratégias através de um conta virtual (conta demo). Isso ajudará a impulsionar o seu confiança na negociação e análise de opções binárias.

Uma conta virtual tem propriedades semelhantes a uma conta real. Porém, uma conta virtual não permite a utilização de dinheiro real, ao contrário de uma conta real.

Você ainda pode investir e ver qual teria sido o resultado se tivesse usado dinheiro real. No final, a possibilidade de ganhar e perder dinheiro real é nula. Portanto, é uma forma de negociação sem risco.

Investidores experientes preferem usar contas virtuais para testar a honestidade do fórum. Desta forma, os traders sabem que as informações apresentadas na plataforma são confiáveis e confiáveis. Ao negociar com dinheiro real, você precisa ter um técnica vencedora sólida. Essas contas virtuais ajudam você a desenvolver suas próprias estratégias. Ter conhecimento completo da plataforma é imprescindível. Por exemplo, algumas opções binárias têm um prazo de validade de meros segundos. Conseqüentemente, reduzir a latência pode significar a diferença entre vitória e derrota.

A conta mínima baixa

Então, agora você tem uma estratégia vencedora confiável e está pronto para começar a investir com dinheiro real. Mínimos baixos são a escolha perfeita para você e qualquer outro iniciante que queira começar a investir dinheiro real. Os investidores que usam a conta mínima baixa podem usar e desfrutar de todos os privilégios de negociação. Mas isso tem um problema. Os investidores que os possuem têm um saldo de conta mais baixo do que o normal.

As contas padrão para opções binárias geralmente têm um saldo em torno de $500. Qualquer valor abaixo dele é representado como uma conta mínima baixa. Porém, essa categorização também pode depender do seu corretor. Esses incluem Conta Micro, Básica ou Iniciante.

Devido ao menor risco envolvido, também traz quedas. Você perderá imensas oportunidades de investimento e outros privilégios. Os correntistas não podem usar alavancagem pela simples razão de não terem fundos suficientes. Também pode causar uma desvantagem quando surgem oportunidades ou opções de alto risco com um período de tempo notavelmente mais curto.

Embora os riscos nestas oportunidades sejam elevados, elas colhem maiores recompensas. Depois de atualizar sua conta, todos esses privilégios e oportunidades de investimento serão adicionados ao seu repertório.

A conta de negociações exóticas:

Você já pensou que seria capaz de negociar quais serão as condições climáticas no Texas daqui a uma semana? As negociações exóticas permitem que você faça exatamente o mesmo. Da determinação do preço às condições climáticas, você pode dar lances em qualquer coisa.

A negociação exótica permite que você dê lances nesses tipos de opções binárias. Por exemplo, você pode fazer lances com base nas condições climáticas futuras de um determinado local ou nas taxas de juros anunciadas pelo Federal Reserve.

A conta de negociações exóticas dá acesso a diferentes tipos de opções, o que se mostra benéfico para sua jornada de investimento.

A lista dos tipos de opções de negociação mais populares é fornecida abaixo:

Alto / Baixo

É o tipo mais básico de negociação de opções binárias. Neste, você analisa um ativo que pode ser uma ação, moeda, mercadoria ou índice. O plataforma então faz uma pergunta:

“O valor do ativo X será maior ou menor que seu preço atual quando o tempo Y expirar?”

Você simplesmente escolhe 'alto' ou 'baixo' com base na sua opinião. Se você estiver correto em sua afirmação e o ativo for negociado exatamente no nível que você emulou quando o tempo acabar, você ganha a oferta. Caso contrário, é uma perda.

Dentro/fora

Pode ser essencialmente denominado como 'negociações duplas sem toque'. Você prenuncia se o preço do ativo permanecerá em uma faixa específica. Se o preço permanecer dentro da faixa especificada quando o tempo expirar, você ganha a negociação e vice-versa.

Escada

As negociações em escadas são relativamente uma invenção mais recente. Pode ser um pouco complicado de executar e obter lucros com isso. A negociação em escada é semelhante às negociações de alta/baixa e One Touch. Você ainda está prevendo em que direção o valor de um ativo irá e dentro de qual prazo.

Embora, nas negociações em escada, você divida a negociação em partes, o que permite obter vitórias e perdas parciais. Geralmente é executado por traders profissionais e pode levar algum tempo para você obter lucros com esse tipo.

Toque/sem toque

O tipo de negociação faz uma pergunta simples:

“Este ativo X alcançará o ponto de gatilho Y no prazo de expiração Z?”

Tudo o que você precisa fazer é simular se ele tocará o ponto de gatilho ou não. Lembre-se de que, em negociações por contato, quanto mais longe o ponto de gatilho estiver do preço atual, maiores serão os pagamentos. É exatamente o oposto de sem toque. Portanto, se sua afirmação estiver correta, você ganha a negociação. Caso contrário, você perderá seu investimento.

A conta profissional

Como o nome sugere, essas contas geralmente são destinadas a traders sofisticados. Esta conta apresenta o maior risco do que qualquer um dos tipos de conta discutidos. Esses investidores têm saldos de contas médios elevados e múltiplas negociações acontecendo simultaneamente.

Os traders profissionais tentam usar essas opções binárias como proteção entre si. Se esta estratégia for utilizada de forma eficiente, pode gerar retornos elevados, mas a utilização indevida pode levar a enormes perdas.

Ele permite que o usuário tenha os mais altos níveis de alavancagem.

Como já mencionado, as contas alavancadas permitem ao trader investir exponencialmente mais do que o saldo da conta existente. Porém, se o investidor perder a negociação, ele pode perder mais do que o valor de sua conta e acabar devendo dinheiro à corretora nesse cenário.

Essas contas permitem que os investidores profissionais acessem toda a gama de negociações. Dependendo do seu estilo de negociação, eles podem participar em negociações de alta frequência ou fazer apostas em qualquer ativos exóticos. Certas corretoras auxiliam os titulares de contas profissionais, prestando atendimento personalizado. Pode incluir um concierge e acesso a materiais educacionais proprietários.

Conclusão: abrir uma conta de opções binárias é fácil e rápido

Dependendo do corretor com o qual você se inscreveu, Opções binárias o registro pode levar de algumas horas a vários dias.

É importante que você observe que, se um corretor não exige a verificação de identidade de uma maneira específica, isso não significa que ele seja menos confiável. A maioria dos corretores de opções binárias são confiáveis e as chances de você se inscrever com um corretor inimigo são muito baixas.

Agora que você sabe como preencher o registro de opções binárias, pode concluir rapidamente o processo de inscrição e começar a negociar.

(Aviso de risco: seu capital pode estar em risco)

Perguntas frequentes sobre a conta de opções binárias:

Quais são os possíveis resultados de colocar um Negociação de opções binárias?

Se o seu prognóstico sobre a direção do movimento dos preços estivesse certo, os lucros estipulados seriam creditados em sua conta.

Se a opção expirar e seu prognóstico estiver errado no vencimento, você perderá o valor investido.

Se não houver alteração no preço, você receberá o valor investido de volta.

Suas perdas são limitadas ao tamanho do valor do ativo.

Tenho que financiar minha conta de negociação no momento do registro?

Você precisará depositar em sua conta pelo menos o depósito mínimo. O depósito mínimo varia de corretora para corretora. Normalmente é $50 ou menos, mas alguns corretores têm um requisito de depósito mínimo mais alto.

Posso negociar opções binárias do meu telefone?

Se o corretor com o qual você se inscreveu tem um aplicativo disponível na Google Play Store ou na App Store, você poderá negociar binários em seu telefone sem muito trabalho. A maioria dos corretores tem sites compatíveis com dispositivos móveis, portanto, você poderá negociar no seu telefone visitando o site no navegador se um aplicativo não estiver disponível.

Posso fechar minha conta de negociação binária mais tarde?

Sim, é fácil excluir sua conta de uma plataforma de negociação. A maioria das plataformas de negociação tem a opção “Excluir conta” em sua página. No entanto, alguns exigem que você entre em contato com a equipe de suporte ao cliente para excluir sua conta.

Quanto dinheiro as contas de demonstração possuem?

Normalmente, as contas de demonstração vêm com 10.000 unidades da moeda de sua preferência. Dito isso, os fundos “padrão” na conta de demonstração variam de plataforma para plataforma.